Get your free credit assessment today, call 385-360-5858

Credit mistakes standing in your way? Let’s fix that

EXCELLENT 4.7 Average Score

Trustpilot TrustScore

Call now to speak with one of our credit specialists and see how easy it is to fix your credit—starting today!

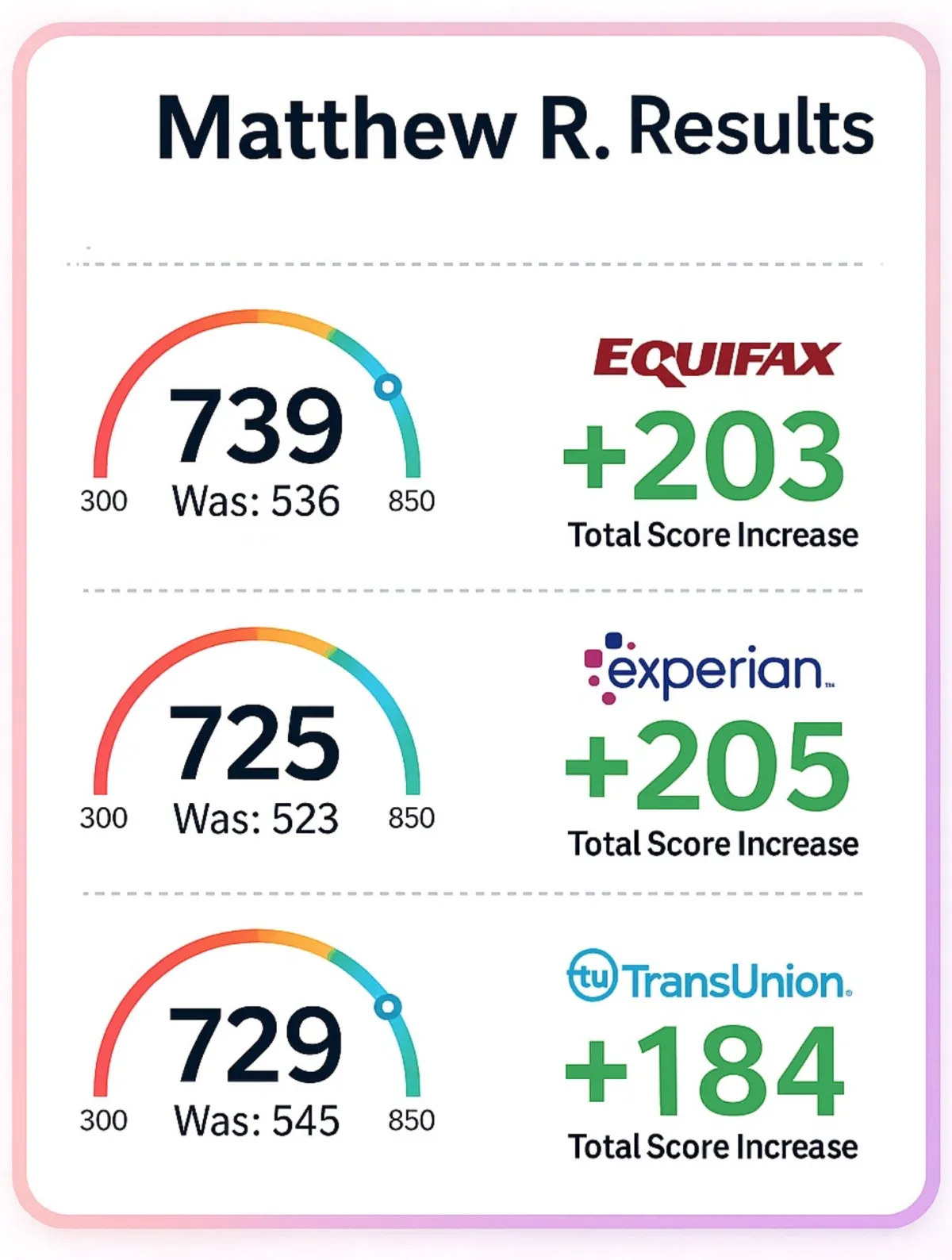

Dispute mistakes on your credit report

A U.S. PIRG study found that up to 79% of credit reports contain inaccuracies or serious errors — we help you correct them.

✔ Collections

✔ Names

✔ Charge-offs

✔ Addresses

✔ Balances

✔ Bankruptcies

✔ Late Payments

Getting started is simple — just three easy steps

1. Speak with a Credit Pro

Have a quick consultation to determine how we can best improve your credit — tailored advice, no time wasted.

2. Start Your Journey

Sign-up is fast and simple. We’ll collect a few details and your credit reports from all three bureaus to get moving.

3. We Go to Work

Our team challenges creditors and bureaus on your behalf, handling every dispute and document so you don’t have to.

Questions? Contact Me

I'm are here to assist you with all of your credit needs. Contact me by phone, email, or via my contact form.

“Really happy with how everything’s been going. My credit scores have steadily gone up over the past few months, and Jessica has kept me in the loop the whole time. She checks in regularly and is always quick to respond whenever I have a question.”

-Gerardo J.

“I was hesitant at first because there are so many credit repair companies out there that promise results and don’t deliver. That definitely wasn’t the case here. They’ve been amazing—my credit score has jumped well over 150 points in a short amount of time. They stay in touch, keep you updated, and are always super helpful. I couldn’t be happier with the results.”

-Tiana A.

© 2026 90 Day Credit Experts

ˣThis is not actual debt, rather debt displayed on a credit report